Story Highlights

- Chinese customers lean more digital than people in the U.S. and other countries

- Rapid digitalization hurts banks' customer relationships and brand differentiation

- Chinese banks should focus more on financial advice than digital expansion

Digitalization is the name of the game in the Chinese financial services industry.

Chinese banking customers lean more digital than banking customers in the U.S. and some other countries do: Almost one in three Chinese banking customers (31%) report using digital banking channels exclusively, compared with 14% of U.S. banking customers.

When it comes to digital wallet usage, China is far ahead of the curve, outpacing the combined of customers in the U.S., Spain, Germany and Argentina. And with the latest world-record sales reported by e-commerce giant Alibaba on China's Singles' Day holiday, one of the largest online shopping days in the world, digital payments in China are expected to soar even higher.

Chinese banking customers' extensive adoption of digital channels is largely related to the rise of financial technology -- or "fintech" -- companies. Across the globe, fintech is shaking up the banking industry, disrupting everything from mobile payments and loans to fundraising and asset management. In the Chinese market, Alibaba and Tencent are key fintech players, leading banks to try to ramp up their digitalization efforts.

Rapid Digitalization Is Hurting Customer Relationships

The trouble is, rapid digitalization is damaging banks' customer relationships and brand differentiation, as many Chinese banks lose sight of what their customers want most. A majority of Chinese customers are not experiencing the meaningful financial relationships they desire from their banks.

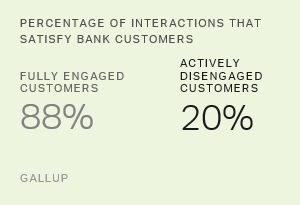

In fact, 23% of Chinese banking customers are fully engaged -- significantly lower than in the U.S. and other Asian countries. Fully engaged banking customers are attitudinally loyal and emotionally attached to their bank -- and, consequently, purchase more products and act as brand ambassadors.

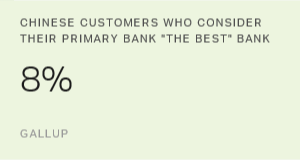

Most Chinese banking customers lack emotional attachment to their bank, seeing it merely as a tool to accomplish tasks. Eight percent of Chinese banking customers consider their primary bank "the best" compared with other banks -- and almost half (46%) feel their primary bank is about the same as other banks.

Because of this low , Chinese banks can expect diminished revenues and customer loyalty, with customers ready and willing to leave for a better deal or for a more convenient fintech company such as WeChat or Alipay. This is no small problem: According to a recent study from Goldman Sachs, the fintech sector is positioned to steal up to from banks.

Gallup's research suggests that Chinese financial leaders should not assume digital offerings and vast omnichannel infrastructures are , even though Chinese customers seemingly prefer digital channels. Among Chinese banking customers, the strongest drivers of customer engagement are assistance with: 1) achieving financial goals and 2) making better financial decisions.

By contrast, the availability of digital devices and the ability to bank any way, anywhere and anytime are far less important than good financial advice. Further, in light of China's recent economic boom, many Chinese banking customers are rapidly accruing wealth -- amplifying their perceived need for financial guidance.

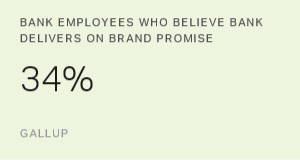

Unfortunately, Chinese banks exhibit the lowest performance on the most important customer engagement drivers: helping customers with their financial goals and decisions. In other words, Chinese banks are struggling to satisfy what is most important in their customers' eyes.

How Chinese Banks Can Deliver What Customers Want

Rather than focusing on aggressive digital expansion and competing with fintech companies to become leaders in technology, Chinese banks need to deliver what their customers really want: financial advice and support. The following best practices can help leaders in this endeavor.

Develop a customer-centric culture. In China, banks have many key performance indicators for sales but fewer for service. Chinese banks need to emphasize service over sales, with every customer interaction.

Managers and leaders should encourage both customer-facing workers and those in support roles to approach their work with customers in mind. The best service is defined not by banks, but by customers.

And addressing what customers want the most is the best way to engage them. This long-term strategy -- with employees at all levels of the company considering customers first -- creates a culture that revolves around customers and fosters customer engagement.

Make every personal interaction count. Especially with , Chinese banks need to capitalize on every in-person interaction. Managers and leaders should equip employees to ask smart questions about customers' financial goals and offer meaningful advice.

Banks cannot afford to wait for customers to ask for help; they need to proactively identify customers' unique financial needs through ongoing conversations and customer analytics. To stay up to date with each customer, banks should keep track of customers' financial goals and periodically consult with customers on their needs.

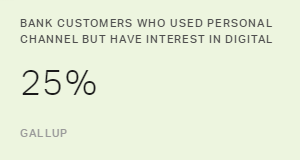

Offer financial advice in self-service digital channels. As almost one in three Chinese banking customers use digital channels exclusively, financial leaders need to seize every opportunity to provide financial advice through digital channels.

For example, banks should provide educational videos or newsletters via online, email and social media channels to address customers' chief financial concerns. Further, banks should strategically position digital education resources, using tactics such as educational kiosks in branches to advise customers waiting in line or audio education for customers waiting to speak to call center representatives.

Leverage employee talents and strengths. To provide customers with exceptional financial advice, leaders need to ensure that all employee-customer interactions leave customers feeling more knowledgeable and confident about managing their finances, clearly conveying the bank's interest in their financial well-being. This requires who can effectively discuss financial topics and craft meaningful, tailored solutions for customers -- rather than simply reciting available products and services.

Financial leaders and managers also need to position employees based on their . For example, employees who are deliberative should help customers manage financial risks, highly disciplined employees should help customers regulate their expenses, and futuristic employees should help customers develop financial goals.

Bailey Nelson contributed to this article.