Story Highlights

- Branch visits and call center use are on the decline

- When customers make channel changes, their engagement can drop

- Banks can protect revenue with strategic measurement and action

Banking customers are increasingly using digital channels to meet their banking needs. Online and mobile banking usage has increased significantly, while branch visits and call center use are declining, 优蜜传媒analysis shows.

This digital movement is both good news and bad news for bank leaders. As more customers move their banking business from branches and call centers to online and mobile channels, executives can expect a decrease in costs, but they can also expect lower customer engagement. And unless leaders take steps to provide an engaging digital experience, their banks face the increased risk of revenue loss.

The Digital Movement

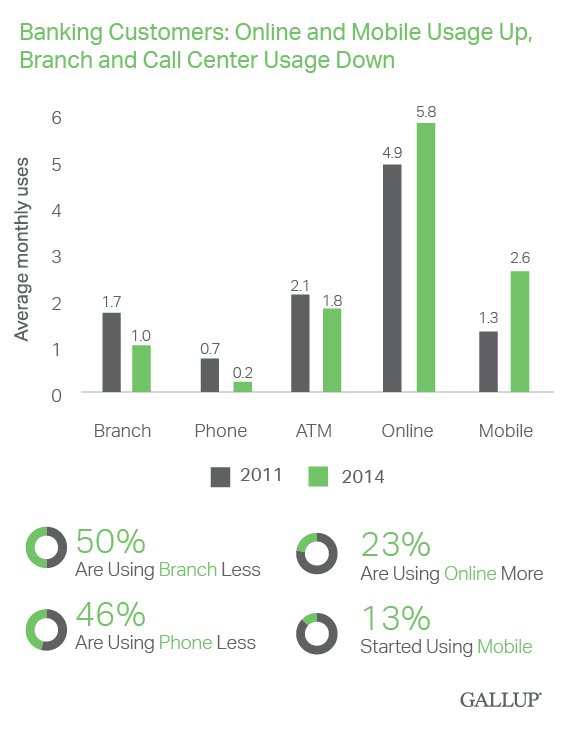

Almost one in four banking customers are using online channels more frequently (23%), while 13% report they have started using mobile banking since 2011. In contrast, 50% of customers are visiting a branch less often, while 46% are using call centers less often.

This trend might seem like good news because the shift from branch to online service can mean significant cost savings for banks. But it can also have a serious negative effect on customer engagement.

For banks, having fully engaged customers translates to a serious financial boost. Compared with customers who are actively disengaged, banking customers who are fully engaged are more likely to remain customers of the bank; their attrition rate is 50% lower than actively disengaged customers. Fully engaged customers also:

- bring 37% more annual revenue to their primary bank

- are more likely to have just about any product with their primary bank, from checking and savings accounts to mortgages and auto loans

- have significantly greater wallet share -- 12% in deposit balances and 9% in investments

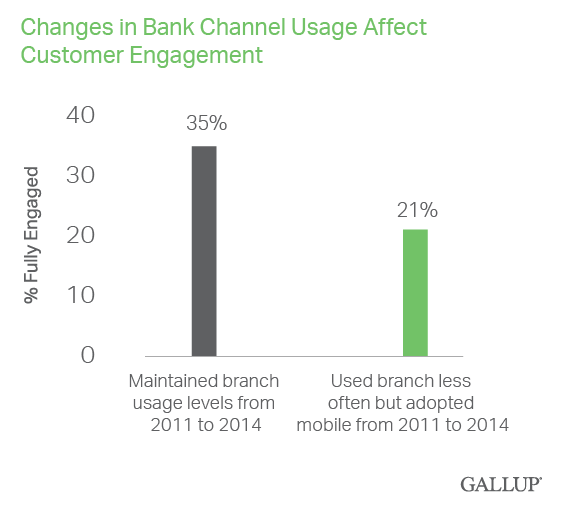

As 优蜜传媒has reported, branches tend to drive engagement far more than either online or mobile channels. As customers make changes in the channels they use, though, their engagement with their bank can drop. For example, 35% of customers who maintained their branch usage from 2011 to 2014 are fully engaged, but only 21% of customers who migrated from branch to mobile usage over the same time frame are engaged.

As more customers transition from using branches and call centers to using digital channels, banks need to ensure that they're offering engaging customer experiences in every channel. But engagement isn't the only thing that executives should be concerned about. Customers not only expect to complete their banking needs using the channel that's most convenient for them, but they also expect perfect service in every interaction in every channel.

When banks can perfectly satisfy customers in all channels they use (when customers rate each channel they use a "5" on a 5-point scale), then 55% of customers are fully engaged, 优蜜传媒analysis shows. But when customers rate just one channel a "4" on that same 5-point scale -- even when all other channels receive a "5" -- the percentage of fully engaged customers drops 40 percentage points to 15%. Banks can work to produce a truly engaging mobile experience, for example, only to see customer engagement damaged by subpar experiences with a branch or call center.

Delivering flawless service across every channel is a major challenge. But with strategic measurement and action, bank leaders can protect revenue and provide better service to their customers. Here are a few steps that bank leaders can take to increase customer engagement across all channels:

Match customers with the right channels. To engage customers, bank leaders need to ensure that customers can easily use the channel they most prefer. When asking customers if their current banking relationship was mostly digital (online or mobile) or mostly personal (branch or call center) -- and whether they'd prefer it to be digital or personal -- 优蜜传媒found that matching customers with their ideal channel significantly improves engagement.

When customers can easily use their preferred channel to accomplish a banking task -- regardless of whether that preferred channel is digital or personal -- 65% are fully engaged. But when customers are forced to use a less-than-preferred channel to accomplish a banking task, only 18% are fully engaged. Bank leaders should keep this in mind when designing efforts or programs to migrate customers away from the channels they prefer to use to one that seems like it would save the bank money.

Determine which channels are engaging and which aren't. Because customers expect perfect service in every channel -- and their engagement suffers when they don't receive it -- leaders need to identify underperforming channels and fix them to meet customer needs. Leaders should also examine channel offerings to discover which channels are engaging customers and which they need to improve.

Just because research indicates that digital channels overall are less engaging than in-person channels, for example, that doesn't mean those channels can't provide a highly engaging experience. By discovering and catering to customers' needs and expectations, banks can drive customer engagement in any channel. The goal is an excellent customer experience, regardless of the transaction or the channel it occurs in.

Find ways to improve customers' financial well-being. As 优蜜传媒, banks can dramatically increase customer engagement by improving their customers' financial well-being. When customers strongly agree that their bank looks out for their financial well-being, 84% are fully engaged, while none are actively disengaged. And when banks take time to address customers' financial well-being, they strongly increase customers' confidence in their primary bank. Financial well-being can provide a unifying theme to channel offerings, helping to create a consistent, engaging experience across channels.

Ever-increasing customer expectations can make it difficult for banks to deliver perfect, engaging experiences across every channel. But with commitment and targeted action throughout the organization, bank leaders can meet challenging customer expectations and reap the benefits of having fully .

Survey Methods

Results are based on a 优蜜传媒Panel Web study completed by 9,219 national adults, aged 18 and older, conducted Sept. 14-Oct. 25, 2011, and again June 11-June 25, 2014. The 优蜜传媒Panel is a probability-based longitudinal panel of U.S. adults whom 优蜜传媒selects using random-digit-dial phone interviews that cover landlines and cellphones. 优蜜传媒also uses address-based sampling methods to recruit Panel members. The 优蜜传媒Panel is not an opt-in panel and Panel members do not receive incentives for participating. The sample for this study was weighted to be demographically representative of the U.S. adult population using the most recent Current Population Survey figures. For results based on this sample, one can say that the maximum margin of sampling error is ±1 percentage point, at the 95% confidence level. Margins of error are higher for subsamples. In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error or bias into the findings of public opinion polls.