Story Highlights

- Digitizing private-sector wage payments especially promising

- In developing countries, 160 million unbanked save informally

This article is the second in a series on global financial inclusion based on data collected in 2014 for the Global Financial Inclusion (Global Findex) database of the World Bank.

The number of adults worldwide who report having an or through a mobile money provider has expanded rapidly in the past few years. However, with an estimated 2 billion adults lacking access to an account, opportunities still exist to increase financial inclusion even more.

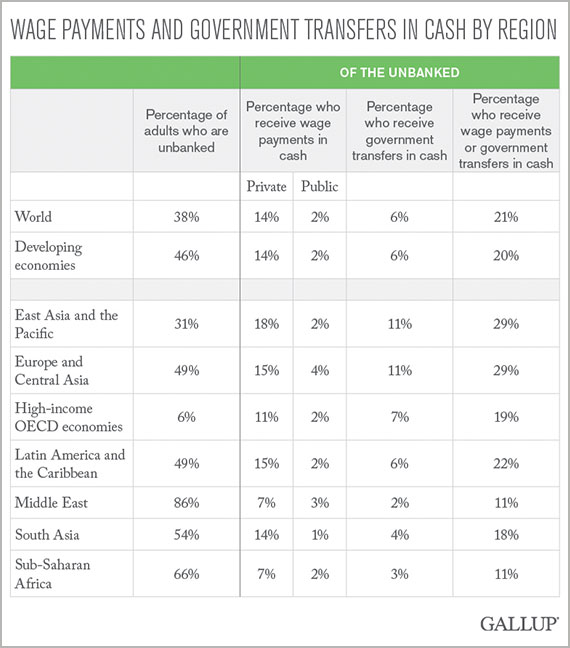

Digitizing the relatively large percentage of payments that are currently being made in cash is one possible avenue to expanding financial inclusion. Worldwide, 21% of unbanked adults -- more than 400 million people -- receive either wages or government transfers in cash.

These results come from the 2014 Global Financial Inclusion () database, which measures the extent of account penetration, the use of mobile money payments and saving and borrowing practices in more than 140 economies. It updates the original Global Findex, which the World Bank launched in 2011 in cooperation with Gallup, and is funded by the Bill & Melinda Gates Foundation.

If governments alone shift the payment of wages from cash into accounts, the number of adults worldwide with an account could increase by as many as 35 million. Doing the same for government transfers such as subsidies, unemployment benefits or payments for educational or medical expenses could increase the number of account holders by up to 130 million. Overall, moving both types of payments into accounts could increase the number of adults with an account by up to 160 million. Among regions, the potential growth from this would be largest in East Asia and the Pacific and in Europe and Central Asia, where 11% of the unbanked in each region receive such payments from the government.

However, the private sector could make an even bigger contribution to further expanding financial inclusion. Globally, 14% of unbanked adults receive private-sector wages only in cash. Paying these through accounts rather than in cash could increase the number of adults with an account by as many as 280 million.

Formalizing Savings Could Create 160 Million New Accounts

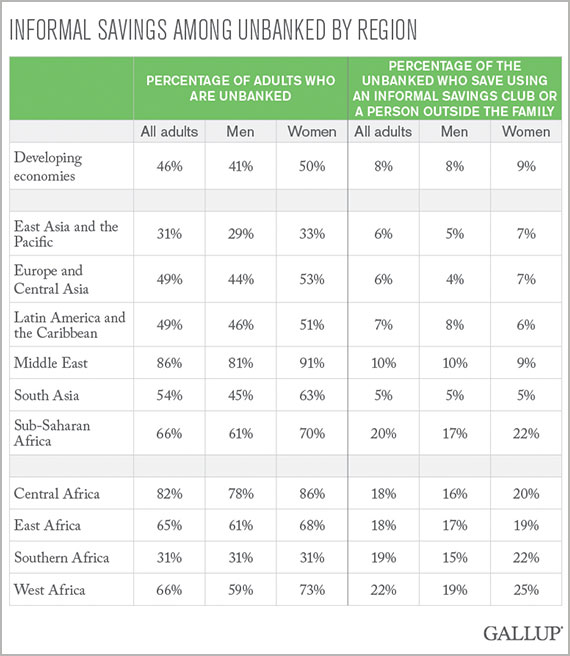

Shifting the non-formal savings of unbanked adults into accounts could also expand financial inclusion. In developing economies overall, roughly 160 million unbanked adults -- 8% of the total in developing economies -- save by using a person outside the family or an informal savings method. This includes rotating savings and credit associations, like tontines and stokvels, which operate by regularly pooling member deposits and disbursing the entire sum to a different member each period. The prevalence of these non-formal saving methods varies across regions, ranging from 5% of unbanked adults in South Asia to 22% in West Africa.

In sub-Saharan Africa, one in five unbanked adults save by using an informal savings club or a person outside the family; shifting these savings into accounts could add up to 70 million adults to the ranks of those with an account. This would disproportionately benefit women. For example, 25% of unbanked women in West Africa save by using an informal savings club or a person outside the family, compared with 19% of unbanked men.

Digitizing Payments Could Improve Efficiency and Reduce Theft

Switching from cash payments to digital payments -- whether these are wages or government transfers -- could have many potential benefits for both senders and recipients. It could improve the efficiency of these payments by increasing their speed and lowering the costs of disbursing and receiving them. Moreover, increased security and transparency of these payments could reduce the likelihood of theft and corruption. Finally, it provides an important first entry point into the formal financial system for those who are currently unbanked.

Such a shift is not without challenges and requires making upfront investments in the payments infrastructure, like increasing the number of points-of-sale terminals and automated teller machines. Moreover, recipients must understand the basic interactions involved in digital payments and be made aware of how accounts work and can be accessed. Unbanked adults can only be brought into the formal financial system if receiving digital payments and using formal savings are as cheap and easy as the alternatives.

Survey Methods

Results are based on telephone and face to face interviews with approximately 1,000 adults per country, aged 15 and older, conducted in 2014 in more than 140 economies. For results based on the total sample of national adults, the margin of sampling error ranged from 卤2.5 percentage points to 卤5.2 percentage points at the 95% confidence level. Margins of sampling error for regions presented in this article tend to be smaller, while those for demographic groups are substantially larger.

.

For more complete methodology and specific survey dates, please review .

Learn more about how the works.