优蜜传媒analysis of confidence in institutions reveals a crisis in the U.S. banking industry. In October 2010, the number of Americans expressing a "great deal" or "quite a lot" of confidence in banks fell to an all-time low of 18% -- lower than its level at the height of the global financial collapse. 优蜜传媒analysts find this to be a continuation of a free fall that began in 2006.

If banks think they can find political cover in the current climate, though, they're sorely mistaken. There appears to be no safe side of the political aisle for financial institutions. The major tenets of the Dodd-Frank Wall Street Reform and Consumer Protection Act received broad support from Democrats and independents and a relatively high level of support from Republicans. Compared with four other major pieces of legislation passed by the 111th Congress -- the economic stimulus, the auto industry and bank bailouts, and the healthcare overhaul -- increased government regulation of banks was the only one that the majority of Americans supported.

Small businesses have lost confidence in banks as well. 优蜜传媒finds that fewer than one in three small-business owners trust banks. This lack of trust is not only a primary contributor to the overall crisis, but it is also likely hindering nationwide economic and job growth.

Confidence breeds loyalty

When 优蜜传媒analyzes consumers' confidence in their primary bank, achieving 50% or more customers who say they have "a great deal" of confidence in their bank is a great result, while any response less than "a great deal" of confidence points to a problem with trust. Consumer confidence levels for large and regional U.S. banks are below that 50% mark. Only 32% of customers of large banks and 40% of regional banking customers express "a great deal" of confidence in their primary bank. (See graphic "Consumer Confidence and Loyalty in Primary Bank.")

Furthermore, banks' efforts to build confidence with small-business customers are also failing. Only 22% of small-business customers of large banks and 24% of small-business customers of regional banks express "a great deal" of confidence in their primary bank. (See graphic "Small-Business Confidence and Loyalty in Primary Bank.")

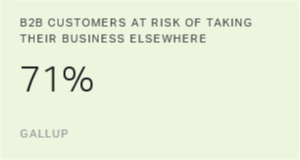

The data for consumers and small businesses also show a strong link between the percentage of customers expressing a great deal of confidence in their primary bank and loyalty to that bank. Yet 优蜜传媒finds that the majority of customers are not committed to their primary banking institution. Approximately three in five consumers -- and four in five small-business customers -- are at risk of defecting to a competitor. The lack of trust small businesses have in banks also contributes to the current low levels of optimism among small-business owners, which in turn affects bank revenue and ultimately, GDP growth.

A crisis of trust

优蜜传媒analysts have discussed this crisis of trust with many bank leaders and have found that rebuilding trust is a top priority for many of them. To date, however, bank leaders' response has been ineffective in changing public opinion. Public confidence continues to decline despite national and regional advertising campaigns, lobbying efforts, community activities, and many other initiatives. Prolonged public distrust has made banking an easy target in Washington, opening the door to further government regulation and vilification of bankers by the public and Congress.

Banks' independence and financial futures depend on increasing trust.

Because levels of trust are so low, there is little margin for error in efforts to restore confidence among banking customers. Any misstep by a notable bank will create sudden and significant repercussions for the entire industry. For example, the reports of so-called "robo-signers" -- bank employees who speedily approved foreclosures without adequate review -- ignited a firestorm among the public and the government. Within days of the initial reporting in the media, Republican and Democratic attorneys general from all 50 states opened investigations into the matter, with nearly half threatening to halt foreclosures from all banks. If trust in banking does not significantly improve, the continued onslaught of regulation could cause banks to lose their ability to operate independently.

For U.S. banks, there is far more to be gained by improving trust than by lawyering up to fight regulation. While pending federal regulations are a significant and legitimate concern, they are primarily a symptom of a root cause: Americans do not trust banks or bankers, causing lawmakers and regulators to side with the will of the people.

But what exactly does trust mean in this context? In banking, trust is more about what a bank is -- how customers feel about banking there -- rather than the products the bank offers. When analyzing the reasons why customers switched primary banks, 优蜜传媒found significant differences between customers with low trust (those who were not emotionally connected to their primary bank) and those with high trust (those who were emotionally connected). Customers with little or no emotional connection to their primary bank switched because of better fees, prices, and products from other banks. Emotionally connected customers, on the other hand, switched because the "soul" of the bank changed -- it was acquired, it took bailout money, its policies were perceived as unfair or inconsistent, or because customers received poor service from the bank.

How to rebuild trust

The effort to rebuild trust must begin with bank leadership, then flow through a bank's employees to customers, the public, lawmakers, and regulators. Every interaction matters. If bank leaders and employees do not demonstrate that they trust their own bank, other stakeholders never will. Because the process of rebuilding trust with the public starts with the bank, 优蜜传媒recommends that bank leaders make rebuilding employees' trust in banks their No. 1 priority. That involves taking these essential steps:

-

Involve managers and employees in the process of reviewing, recasting, and restating the mission and purpose of the organization.

-

Start with the top 100 managers and cascade the new mission down to the front lines.

-

Align managers on your bank's brand promise and the points of difference between your bank and your competitors.

-

Create metrics to map trust and brand message alignment with key constituencies, including leaders, employees, customers, and regulators.

Focus on small business

Once banks have restored a measure of trust among employees, they need to turn their attention to their customers. Small-business customers in particular must be tended to, as nearly 8 in 10 of them are vulnerable to switching.

Though the relationship between banks and small businesses has never been more fragile, this is arguably the best time ever for banks to expand their small-business portfolios. Collectively, as the nation's largest employer, small businesses fuel job creation and economic growth far more than big businesses do. This is why 优蜜传媒recommends aligning your bank's strategy to help small businesses win.

By stimulating small-business growth and subsequently job creation, banks can create unlimited positive stories for virtually all stakeholders and the whole world. More than ever, bank leaders have the opportunity to influence their future and the world economy. There is little room for error, and there is no political safe haven. Banks' independence and financial futures depend on increasing trust.

The two most effective actions bank leaders can take are increasing employees' trust and helping small businesses win. This is a vision that employees, customers, the public, lawmakers, and regulators will get behind. It is good for business. It is good for the country. It is good for the world.