Story Highlights

- 15-year high 57% of nonretirees anticipate comfortable retirement

- 57% of retirees rely on Social Security as major source of income

- 33% of nonretirees expect to rely on Social Security as major source

WASHINGTON, D.C. -- Nonretired Americans' expectations that they will live comfortably in retirement are more positive than they have been since 2004 suggesting that the public's recent upbeat view of the nation's economy and their personal finances is coloring their retirement outlook. Yet, while overall retirement expectations may be rosier, only one-quarter of Americans who are employed or have an employed spouse say they are currently saving enough for retirement.

Nonretirees, many of whom have known for years that the Social Security system could run out of funds before they retire, remain far less likely than those who have already retired to say they will rely on Social Security as a major source of retirement income.

More Nonretirees Expect to Live Comfortably in Retirement

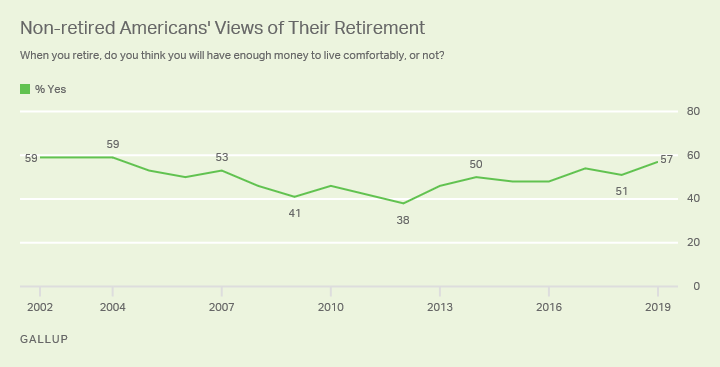

A near record high 57% of nonretired Americans now expect that they will have enough money to live comfortably in retirement while 41% do not. This latest reading, from an April 1-9 ���۴�ýpoll, marks a six-point increase in positivity since last year.

Results on this measure since the first reading in 2002 have generally risen and fallen based on the performance of key economic indicators, including the stock market, the unemployment rate and the housing market. The lowest positive point was 38% in 2012, but it had been low since 2008 as a result of the Great Recession. Since then, expectations have rebounded and now nearly match the historical 59% highs seen in 2002-2004.

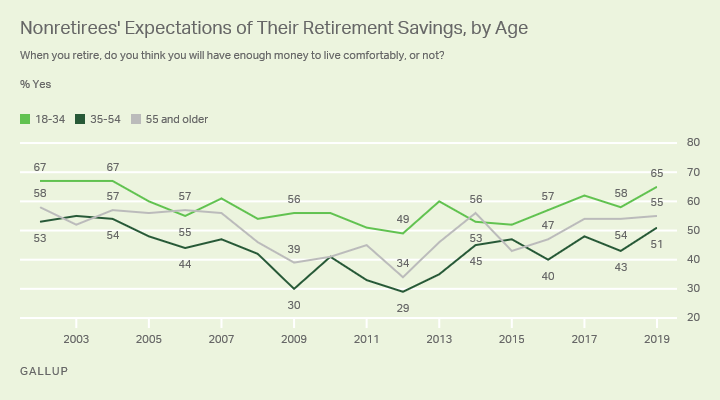

As has been the case historically, younger adults are more confident than their older counterparts when it comes to nonretirees' outlooks for a comfortable retirement, presumably because they have more time to save for it. The latest results find that 65% of 18- to 34-year-olds foresee living comfortably in retirement, compared with 51% of 35- to 54-year-olds and 55% of those closest to retirement, aged 55 and older.

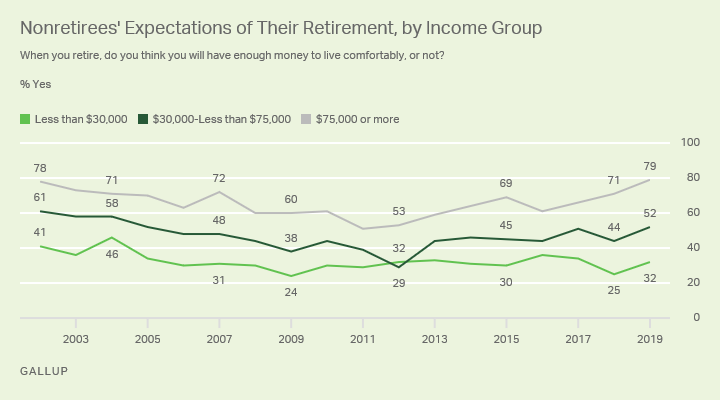

As would be expected, those with higher household incomes are more likely than those in lower income groups to anticipate a comfortable retirement. While 79% of nonretirees with household incomes of $75,000 or more currently think they will be financially secure in retirement, far fewer in lower income brackets -- 52% of those from households earning $30,000 to $75,000 and 32% with incomes under $30,000 -- agree.

Retirement Preparedness Falling Short

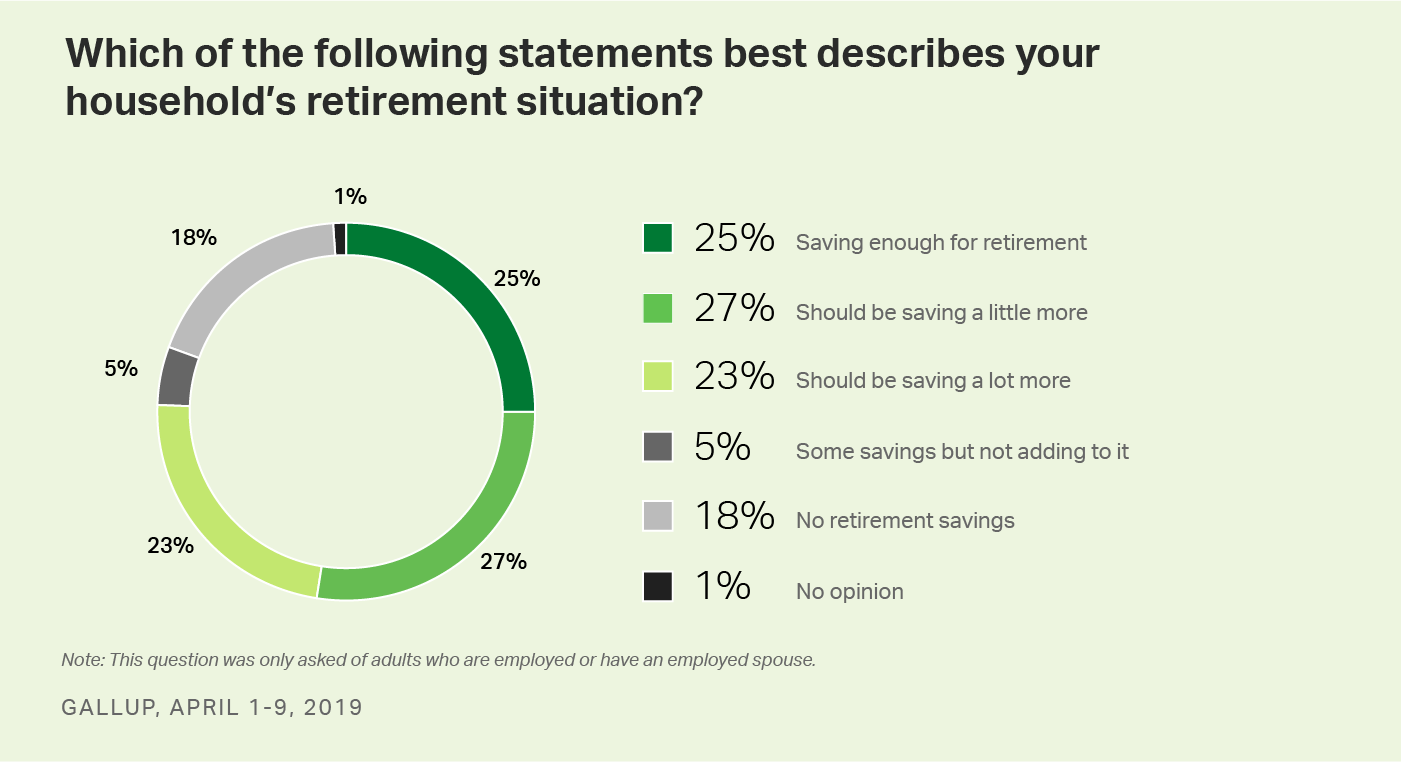

Although nonretirees' retirement outlooks have become more sanguine this year, those who are still employed or have an employed spouse are strikingly lacking in their financial planning for their golden years. These Americans are largely divided in describing their household's retirement situation, with just 25% overall saying they are saving enough for retirement. Half think they should be saving more (27% a little more and 23% a lot more), while 18% do not have any retirement savings and 5% do but are not adding to it. In all, this means 46% of these adults could be classified as largely unprepared for retirement.

These findings, from Gallup's April 17-30 poll, flesh out data from the poll earlier that month which found that while Americans' views of their personal financial situation are largely positive, not having enough money for retirement is among the most worrisome of eight financial issues measured.

This question was asked once before, in 2001, with similar results, which suggests that Americans do not appear to be in a better or a worse situation for retirement than they were then.

Expected and Actual Retirement Age and Fund Sources

Americans today are living longer, working later in life and are less likely to receive a pension from their employer. These realities, along with the potentially perilous state of the Social Security system, shape the way that retired and nonretired Americans plan for retirement.

Delaying retirement: The mean age that nonretirees expect to retire is 65 years old and the actual mean age that retirees report having retired is 61 years old. Both are in line with their trends since 2002, although the percentage of nonretirees who plan to retire over the age of 65 (34%) has fallen to its lowest point since 2010.

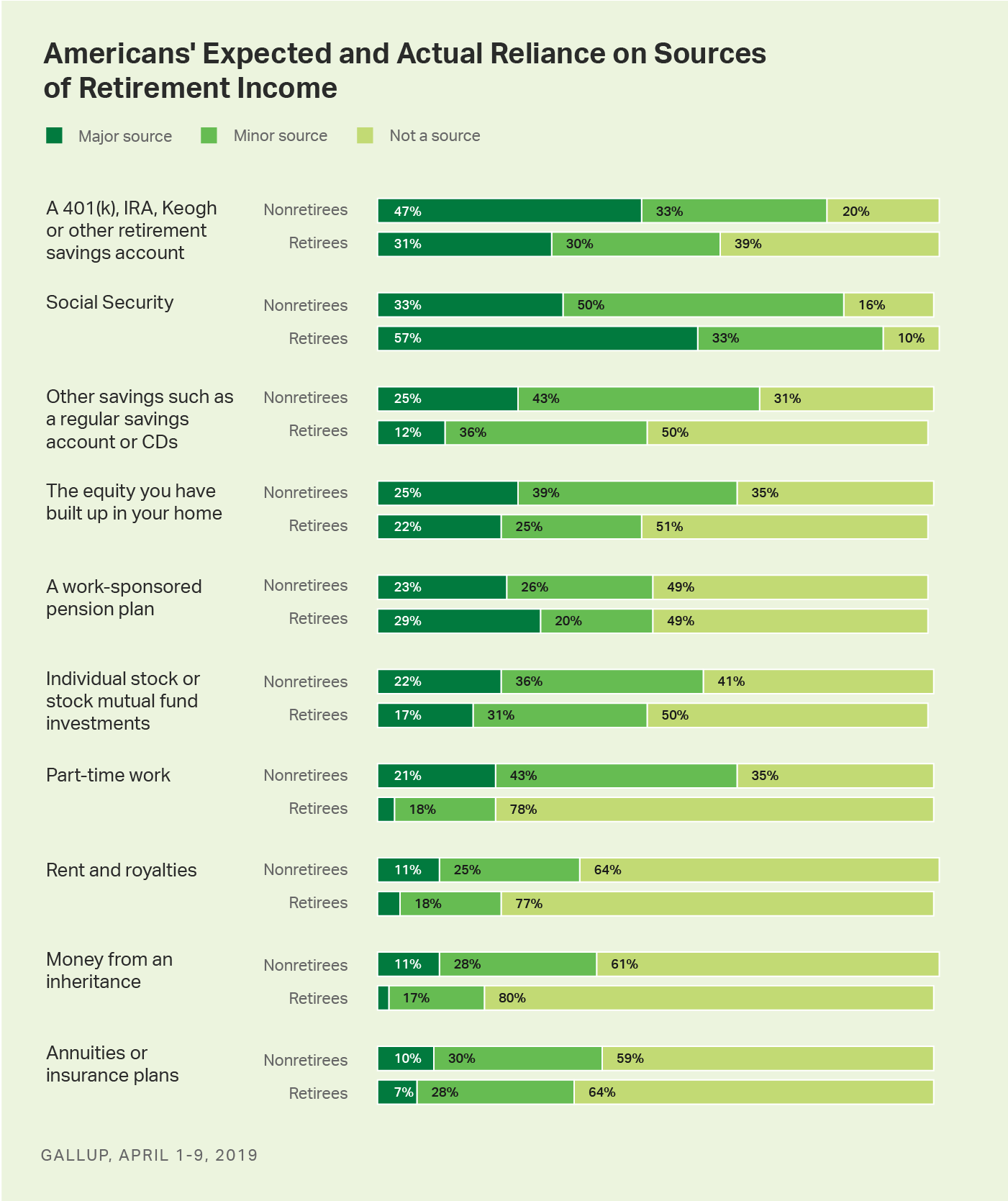

Downplaying reliance on Social Security: Nonretirees and those who have already retired view various retirement income sources very differently. Of the 10 retirement income sources measured in the early April poll, Social Security is by far the most relied upon among retirees, with 57% describing it as a major income source for them. Only 33% of those who have not yet retired describe it the same way.

Putting their eggs in the 401(k) basket: Nonretirees are most likely to say they will rely upon a 401(k), IRA or other similar retirement savings accounts in retirement, with 47% saying it will be a major income source for them. In contrast, such retirement savings accounts are only considered a major source for 31% of retirees.

Counting on a paycheck: Nonretired Americans continue to believe that part-time work will be a significant income source in retirement much more so than those who have already retired (21% vs. 3%), and they are also twice as likely as retirees to expect to rely significantly on other types of savings accounts (25% vs. 12%).

Squeezing money from other sources: Nonretirees are also more likely than those who have already retired to plan to rely on several revenue streams as at least a minor source -- home equity, rent and royalties, and money from an inheritance. Retired adults may have already downsized their homes, sold their investment properties and collected any inheritance money which could account for these differences.

Meanwhile, the expectations of nonretirees and the reality for retirees are fairly similar for the remaining sources of retirement income, including work-sponsored pension plans, stocks, annuities or insurance plans. Retirees' reliance on pension plans as a main income source currently match the 29% historical low last seen in 2002.

Bottom Line

As the U.S. economy continues to hum along and Americans are feeling generally positive about their personal finances, more nonretired Americans expect to be financially secure in retirement now than a year ago.

Those who haven't retired yet say they are largely falling short of where they think they should be with their retirement savings. Now, as America's baby boomers continue to retire and live longer than prior generations, the Social Security trust fund is expected to run out of money in 15 years if lawmakers don't act. Nonretirees seem aware of the challenges facing Social Security, and just one-third of nonretirees currently view Social Security as a major source of retirement income. Nonretirees are instead planning for personal investments and other sources of money to carry them through their later years.