Story Highlights

- Vast majority of investors believe buying home helped their finances

- Identity theft and illness are most financially negative life events

- Older investors more likely to see having children as fiscally positive

WASHINGTON, D.C. -- Buying a home and getting married, the two most common life experiences of U.S. investors, also rank among the top three for having a positive rather than negative effect on investors' personal financial situations. This combination positions marriage and homeownership as the leading positive life events for most investors.

The third-quarter Wells Fargo/优蜜传媒Investor and Retirement Optimism Index survey, conducted Aug. 13-20, determined the impact of various life events by asking investors if any of 14 events had happened to them and, if so, how it impacted their personal finances.

优蜜传媒and Wells Fargo define U.S. investors as adults with $10,000 or more invested in stocks, bonds or mutual funds, either within or outside a retirement savings account.

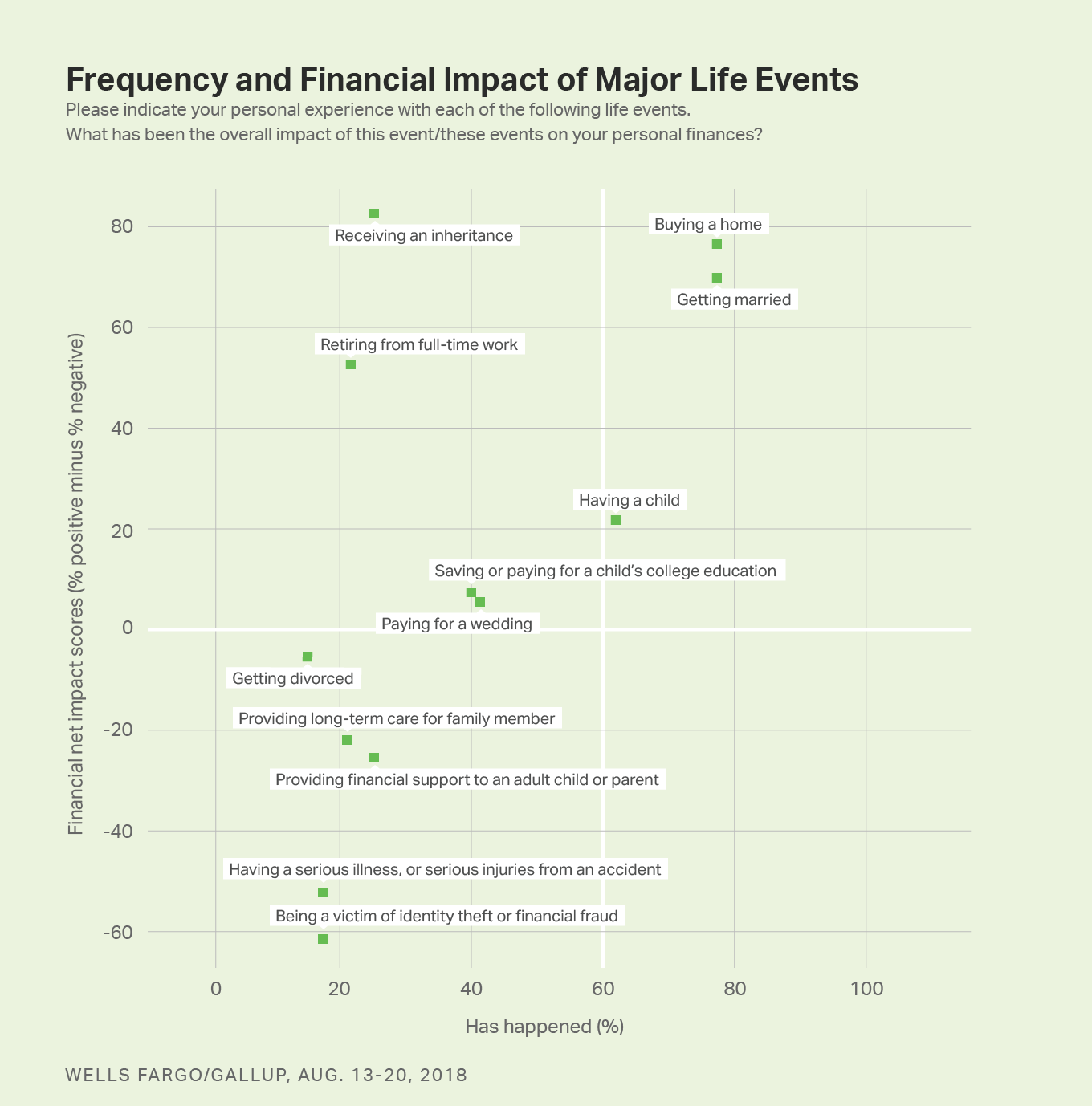

The above graph plots 12 of the 14 events on the survey, displaying the prevalence and net financial impact of each situation. Prevalence is defined as the percentage of investors who say the event has happened to them. The net impact score is the difference between the percentage of investors who say an event has had a very or somewhat positive impact on their personal finances and the percentage of investors who say the event has had a very or somewhat negative impact. A positive net impact score indicates that more investors thought the experience was financially helpful than harmful, while a negative score indicates a larger share found the encounter financially harmful.

Two of the events -- sustaining major property damage or loss from a natural disaster and becoming a widow or widower -- were too uncommon among U.S. investors for 优蜜传媒to be able to report the net impact score of the occurrences. Consequently, they do not appear in the graph.

Buying a home and getting married are the most common experiences that investors have. The events are equally likely, with 77% of investors saying they have bought a home or gotten married. Both events also are seen as a positive financial development.

More than eight in 10 investors who have bought a home (84%) say the overall impact of this action was positive on their personal finances, compared with 7% who say it had a negative impact, for a net impact score of +77. This is the second-highest financial net impact score.

The net impact score of getting married is only slightly lower, at +70.

Older Investors See Child-Related Costs More Positively Than Younger Do

There is less consensus concerning the financial impact of costs typically associated with parenthood, including having a child, saving or paying for a child's education, and paying for a wedding.

Having a child, an action that 62% of investors have done, is seen the most positively of the three. A slight majority (53%) say having a child had a positive impact on their personal finances, compared with 32% who believe the experience worsened their financial situation, for a net score of +21. The emotional aspect of having a child may affect how investors perceive the financial impact.

The net impact scores for paying for a wedding (+7) and saving or paying for a child's college education (+8), each experienced by about four in 10 investors, are closer to a zero score, suggesting a split decision among investors about the sentiments related to the events' financial impact.

For younger investors, such as some young adults or middle-aged investors, these situations may constitute an ongoing financial obligation. For investors 65 and older, these life events are likely in the rearview mirror, at least in a financial sense. Some older investors may now be seeing a return on investment of some sort -- through their child's successful career or fruitful marriage, for example -- that younger investors have not yet observed. These various situations may be why the age groups have differing perspectives on the events: The oldest group of investors is more likely than their younger counterparts to assess the financial impact of all three items more positively.

| 18-49 | 50-64 | 65+ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Having a child | +7 | +23 | +51 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Paying or saving for a child's education | +11 | -13 | +35 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Paying for a wedding | -3 | +7 | +29 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Among investors who say event has happened to them | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wells Fargo/Gallup, Aug. 13-20, 2018 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Retiring and Inheriting Seen Positively, but Not Widely Experienced

Investors who have received an inheritance or retired from work are very likely to believe their experience was a boost to their finances. But these situations describe comparatively few investors: 25% have received an inheritance, and 22% have retired from work.

Not surprisingly, the financial net impact score of receiving an inheritance is higher than that of any other event, at +82.

Retiring from work also has a decisively positive net impact score at +53.

Despite this broadly upbeat assessment of the financial effects of retirement, past 优蜜传媒research found that fewer than half of retirees are highly confident they will have enough money to maintain their preferred lifestyle in retirement.

Though a minority of investors have experienced receiving an inheritance or retiring, many expect they eventually will, particularly with respect to retirement. Beyond the 22% of investors who have retired from work, another 9% expect to retire in the next few years, and 54% expect to retire someday.

About as many investors expect to receive an inheritance someday as say they already have -- 27% and 25%, respectively, for a combined 52% likely to benefit from this financial experience.

Identity Theft and Having Serious Illness Viewed Most Negatively

The life events that were most clearly seen as financially harmful include being a victim of identity theft or financial fraud, becoming seriously ill or injured, and financially supporting an adult child or elderly parent. However, none of these are common occurrences.

A substantial share of investors expect to experience some of the more financially severe misfortunes. Fewer than one in five investors (17%) say they have been a victim of financial fraud or identity theft, an experience that has the lowest net impact score at -61. An additional 31% of investors expect to be a victim of this type of crime in the future.

Likewise, 36% of investors believe they will become seriously ill or injured, an experience that has a net impact score of -52 based on the sentiments of the 17% of investors who have had the experience already.

Despite the financial dangers inherent in both identity theft and medical setbacks, most investors dealing with either of these issues say they did not seek the assistance of a professional financial adviser. Nineteen percent of investors who were victims of identity theft or fraud and 10% of investors who became ill or injured sought counsel from an adviser.

Other events that investors consider financially challenging, if less starkly so than the previous two, include financially supporting an adult child or parent, and providing long-term care for a sick, disabled or elderly family member. This poll found that one-quarter of investors provide financial resources to an adult child or parent, with most of these seeing this arrangement as a financial drag, as signaled by a net impact score of -25.

The net impact score of caring for a sick family member, which 21% of investors have done, is -22.

Bottom Line

The unpredictable nature of life can create financial challenges, as well as opportunities. Furthermore, a person's goals, such as those for one's family or career, may not align neatly with their financial objectives.

But, for two key life events, no such tension exists -- at least for most U.S. investors. The vast majority of U.S. investors have bought a home and/or gotten married, and the investors see those decisions as financially wise. This may be welcome news to the many Americans who expect to tie the knot or buy a home someday.

Other types of life events that tend to be socially celebrated but have clear monetary costs, such as having a child or paying for that child's education, may, in the long run, prove helpful to a person's financial situation, as suggested by older investors' more-positive assessments of these types of events, compared with younger investors.

At the same time, a few life events -- particularly experiencing identity theft or fraud and having a serious illness -- are so unequivocally negative that investors may want to think about measures to avoid or prepare for them.