Story Highlights

- Nearly six in 10 retirees rely on Social Security as major income source

- Pensions rank distant second with 35% relying on them

- Nonretirees put somewhat more emphasis on 401(k) type plans

WASHINGTON, D.C. -- Retired U.S. adults are relying on a number of income sources in their golden years, although Social Security is the only one a majority (57%) calls a "major source." Work-sponsored pensions and 401(k) or other personal retirement savings accounts rank a distant second and third. Fewer than one in five rely on any of several other sources, including home equity, regular savings accounts and part-time work.

| Major source | Minor source | Total source | Not a source | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| % | % | % | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Social Security | 57 | 33 | 90 | 10 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| A work-sponsored pension plan | 35 | 22 | 57 | 42 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| A 401(k), IRA, Keogh or other retirement savings account | 27 | 34 | 61 | 38 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| The equity you have built up in your home | 19 | 29 | 48 | 52 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other savings such as a regular savings account or CDs | 17 | 42 | 59 | 40 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Individual stock or stock mutual fund investments | 15 | 30 | 45 | 54 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Annuities or insurance plans | 9 | 20 | 29 | 71 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Money from an inheritance | 7 | 15 | 22 | 78 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Part-time work | 3 | 15 | 18 | 82 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Rent and royalties | 3 | 15 | 18 | 81 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gallup, April 2-11, 2018 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Even if retirees don't describe an income source as a major source in their retirement, many describe them as minor sources. As a result, more than half of retirees benefit at least to some degree from a 401(k), other savings, or a pension, in addition to Social Security. Roughly half tap into home equity or stock investments. But even on this basis, less than a third get income from annuities, an inheritance, part-time work or rent/royalties.

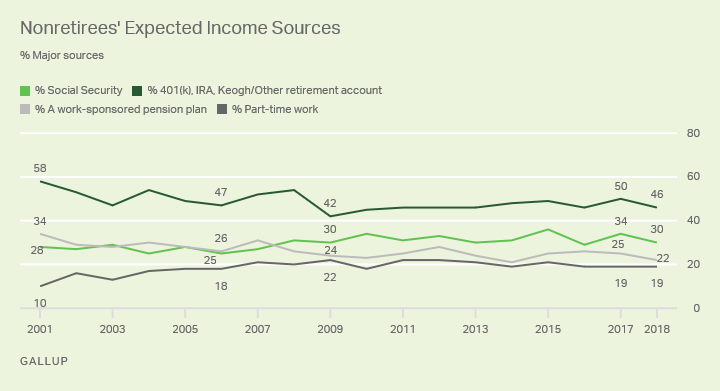

These findings, from Gallup's April 2-11 Economy and Personal Finance survey, are broadly similar to what the poll has shown since 2001. A key exception is that retirees are now more likely to report that a 401(k) or other retirement account is serving as a major income source for them. The 27% rating it a major source today compares with 19% when 优蜜传媒first measured this in 2002. Meanwhile, Social Security has maintained its place at the top of the list of major income sources every year.

Nonretirees Focused Mainly on 401(k)s

Americans who are not currently retired and retirees have significantly different perceptions of how much they will rely on the various income sources. Close to half of nonretirees think a retirement savings account such as a 401(k) will be a major income stream for them in retirement -- the most of any source -- while only 30% predict Social Security will be this important.

The remaining rank order is similar to what retirees report they are actually using, except that nonretirees are more likely than retirees to identify part-time work as a major source (19% vs. 3%, respectively).

| Perceptions of Major Income Sources | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Nonretirees' Expected Income Sources: | Retirees' Reported Actual Income Sources: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 401(k) or other retirement account (46%) | Social Security (57%) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Social Security (30%) | Work-sponsored pension plan (35%) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other savings or CDs (23%) | 401(k) or other retirement account (27%) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Work-sponsored pension plan (22%) | Home equity (19%) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Home equity (22%) | Other savings or CDs (17%) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Stocks or stock mutual funds (19%) | Stocks or stock mutual funds (15%) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Part-time work (19%) | Annuities or insurance plans (9%) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Annuities or insurance plans (8%) | Inheritance (7%) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Rent and royalties (8%) | Part-time work (3%) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Inheritance (7%) | Rent and royalties (3%) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gallup, April 2-11, 2018 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Nonretirees Attaching Less Import to Pensions, More to Part-Time Work

Nonretirees' perceptions of how much they will rely on the various sources have been fairly stable in recent years. Longer term, since 2001, they have become less likely to predict a 401(k) or pension plan will be a major income source for them in retirement, while the percentage expecting part-time work to be this important has almost doubled, from 10% in 2001 to 19% today.

The percentage of nonretirees expecting to rely heavily on Social Security increased during the 2007-2009 recession -- possibly reflecting concern over reduced stock values -- and remained high for several years. But this year's 30% projection of Social Security as a major source of income in retirement is back close to where it was at the start of the trend in 2001.

The differences between nonretirees' and retirees' responses about retirement income sources are also evident in an analysis that follows one group of people from their later working years into retirement. Nonretired adults who were 50 to 64 roughly 15 years ago but who are now 65 or older and retired are much more likely today to say that Social Security is a major source of income for them in retirement than thought that would be the case before they retired, 61% vs. 37%. At the same time, members of this group are significantly less likely as retirees to be relying on home equity, part-time work, or a 401(k) or other retirement savings account than they expected to before retirement.

| Expected use in retirement | Actual use in retirement | Gap | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Age 50-64 in 2002-2004 | Age 65-80 in 2016-2018 | pct. pts. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| % | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Social Security | 37 | 61 | +24 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| A work-sponsored pension plan | 31 | 36 | +4 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Annuities or insurance plans | 5 | 8 | +3 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other savings such as regular savings account or CDs | 11 | 14 | +2 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Rent and royalties | 6 | 6 | 0 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Money from an inheritance | 6 | 5 | -1 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Individual stock or stock mutual fund investments | 19 | 14 | -5 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| The equity you have built up in your home | 27 | 21 | -6 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Part-time work | 14 | 3 | -11 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 401-K, IRA or retirement savings account | 38 | 23 | -15 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gallup | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

This analysis helps document the consistent tendency for Americans to discount Social Security when looking ahead to retirement -- even as Social Security becomes an important source of income once they do retire. Similarly, Americans' optimism about being able to live comfortably in retirement increases from 51% before retirement to 78% once they are retired.

Bottom Line

Social Security remains the bedrock of seniors' financial security, with the solid majority depending on it as a major income source. This has held firm over the past 18 years. At the same time, with ongoing reports that the solvency of Social Security is in jeopardy, nonretirees have, for almost two decades, remained fairly skeptical of how important Social Security will be in their retirement. Far fewer nonretirees predict it will be a major source of retirement income for them than current retirees say it is for them today.

Such pessimism about Social Security may be helpful for nonretirees if it motivates them to increase retirement savings from other sources. To date, nonretirees' 401(k) or other retirement plans have not emerged as a complete substitute, as fewer than half, including 46% this year, say that a 401(k) or other retirement savings account will be a major retirement income source for them. Whether that's because they don't have access to such accounts or because they can't afford to save isn't clear.

The good news is that most retirees end up being financially comfortable when they do retire, in part because of Social Security. This means that nonretirees' best hope could be for the nation's leaders to come together soon to provide the adjustments Social Security needs in order to ensure seniors continue to receive what's owed to them from their working years.

Survey Methods

Results for this 优蜜传媒poll are based on telephone interviews conducted April 2-11, 2018, with a random sample of 1,015 adults, aged 18 and older, living in all 50 U.S. states and the District of Columbia. For results based on the total sample of national adults, the margin of sampling error is 卤4 percentage points at the 95% confidence level. All reported margins of sampling error include computed design effects for weighting.

Each sample of national adults includes a minimum quota of 70% cellphone respondents and 30% landline respondents, with additional minimum quotas by time zone within region. Landline and cellular telephone numbers are selected using random-digit-dial methods.

View survey methodology, complete question responses and trends.

Learn more about how the works.