Story Highlights

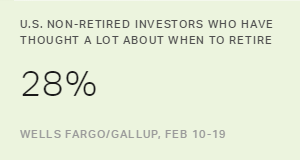

- 28% of non-retired U.S. investors have thought a lot about when to retire

- Most want to retire before 67, the age for full Social Security benefits

- About half have "crunched the numbers" to estimate retirement income

WASHINGTON, D.C. -- Less than a third (28%) of non-retired investors in the U.S. have given a lot of thought to the best age for retirement, while 11% say they have given it no thought and 31% have thought about it only a little. Even among those aged 50 and older, only 39% have thought about it a lot, while 29% have thought about it only a little or not at all.

| A lot | A fair amount | Only a little | None | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| % | % | % | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| All investors | 28 | 30 | 31 | 11 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Age | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 18-49 | 20 | 29 | 38 | 12 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 50 and older | 39 | 31 | 21 | 8 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Amount invested | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than $100,000 | 19 | 30 | 37 | 15 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $100,000 or more | 37 | 30 | 27 | 5 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wells Fargo/优蜜传媒Investor and Retirement Optimism Index, Feb 10-19 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

A majority of those aged 50 and older have not thought a lot about the best age to retire, but the 39% who have done so is nearly double the percentage of investors aged 18-49 (20%) who have given the matter a lot of thought.

Non-retired investors' responses also differ greatly based on how much they have invested. Of those who currently have less than $100,000 in investments, 19% have thought a lot about the best age to retire, while 52% have thought about it a little or not thought about it. Among those with $100,000 or more invested, 37% have thought a lot about when to retire.

These data come from the Wells Fargo/优蜜传媒Investor and Retirement Optimism Index, conducted February 10-19. The index is a survey of U.S. investors who report having $10,000 or more in stocks, bonds, mutual funds, or a self-directed IRA or 401(k). "Non-retired investors" includes all respondents in the survey who identify themselves as not retired, including students, homemakers and those seeking work.

Among retired investors included in the survey, more than half (52%) say they wish they had started to think about the best age to retire earlier.

Most Want to Retire Before Social Security's Full-Benefits Age of 67

Sixty-three percent of non-retired investors want to retire before they reach the age of 67 -- the minimum age to receive full Social Security benefits. But about one in five (23%) don't want to retire and start collecting Social Security benefits until they are at least 70 years old.

Respondents' average expected retirement age of 65 is also the age non-retired investors name most often (27%) as the best age to retire and has a long history as the traditional retirement age. Retirement pension plans, whether from the government or a private workplace, typically started at age 65 throughout most of the 20th century, and Social Security benefits kicked in for all beneficiaries at age 65 from the program's beginning in 1935 until 1983.

Non-retired investors aged 18-49 are more likely to favor retiring before they reach 65 (38%) than are older non-retired investors (23%). One factor explaining this difference is that there are more investors who have already retired among those aged 50 and older than among those aged 18-49.

Most Have Taken Steps to Help Decide When to Retire

Of seven possible actions that can help determine the best retirement age, the one non-retired investors take most often (63%) is discussing the topic with trusted friends or family members. Non-retired investors are least likely (30%) to have reviewed retirement options on the Social Security Administration's website.

Non-retired investors aged 50 and older are more likely than those aged 18-49 to have taken six of the seven steps that could help them determine the best age to retire -- the only exception being the use of online tools to estimate retirement income. The largest gap between younger and older non-retired investors exists for reviewing the Social Security Administration website; 48% of those 50 and older have done so, compared with 18% of those aged 18-49.

| Total | Less than $100,000 | $100,000 or more | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| % | % | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Discussed it with trusted friends or family | 63 | 59 | 68 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Manually "crunched the numbers" to estimate retirement income | 51 | 39 | 62 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Used online tools to estimate retirement income | 50 | 46 | 54 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Talked about retirement with a professional financial adviser | 47 | 35 | 60 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Read up on retirement using financial magazines or websites | 44 | 39 | 48 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Reviewed options on Social Security Administration website | 30 | 23 | 37 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wells Fargo/优蜜传媒Investor and Retirement Optimism Index, Feb 10-19 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Those with at least $100,000 invested are more likely than those with less than $100,000 invested to have taken each of the seven possible actions. The gaps are largest between these groups for talking about retirement age with a professional financial advisor (25 percentage points) and manually "crunching the numbers" to estimate retirement income (23 points).

Bottom Line

The dynamics of retirement are undergoing a fundamental transformation in the 21st century, with more flexibility around when to retire and less certainty about financing it. Nevertheless, one of the key decisions facing non-retired investors is still when they should retire. That choice helps investors determine the amount of risk they should be taking in their investments, how many years they have to save and how much they must save in each of those years to meet their retirement goals.

However, most U.S. investors -- regardless of age or investment value -- have not given a lot of thought to when they will retire, nor have many read up on retirement-age considerations, reviewed the Social Security Administration's website or talked about retirement age with a professional financial adviser. Even among those aged 50 or older, only about half of U.S. investors have taken these steps.

Survey Methods

Results for the Wells Fargo/优蜜传媒Investor and Retirement Optimism Index survey are based on questions asked Feb. 10-19, 2017, on the 优蜜传媒Daily tracking survey, of a random sample of 643 non-retired and 369 retired U.S. adults having investable assets of $10,000 or more.

For results based on the 643 non-retired investors, the margin of sampling error is 卤5 percentage points at the 95% confidence level. For results based on the 369 retired investors, the margin of sampling error is 卤6 percentage points at the 95% confidence level. All reported margins of sampling error include computed design effects for weighting.

Each sample of national adults includes a minimum quota of 70% cellphone respondents and 30% landline respondents, with additional minimum quotas by time zone within region. Landline and cellular telephone numbers are selected using random-digit-dial methods.

Learn more about how the works.