This article is the second in a two-part series on global financial inclusion based on data collected for the World Bank Global Financial Inclusion (Global Findex) database.

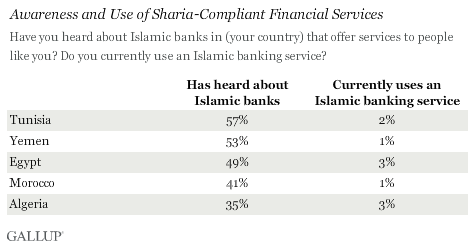

WASHINGTON, D.C. -- In four North African countries -- Algeria, Egypt, Morocco, and Tunisia -- as well as in Yemen, no more than 3% of adults say they currently use a Sharia-compliant banking service.

These results come from a 优蜜传媒World Poll survey conducted in 2012 to supplement the World Bank Global Financial Inclusion (Global Findex) database with an additional questionnaire on the awareness, use, and preference for Islamic financial products. Banks that offer Islamic financial products are profit-maximizing intermediaries between savers and investors and offer custodial and other traditional banking services. Compared with conventional banks, Islamic banks are constrained by Islamic law, also known as Sharia, which prohibits fixed or floating payments or the acceptance of specific interest or fees for loans of money.

Across the five countries surveyed, about half (48%) of adults report having heard of Islamic banks in their country. Awareness ranges from 35% in Algeria to 57% in Tunisia. Among respondents who report having an account at a formal financial institution or having borrowed from a formal financial institution in the past year, 8% identify as current users of Islamic banking services.

Price Influences Preferences for Sharia-Compliant Banking Products

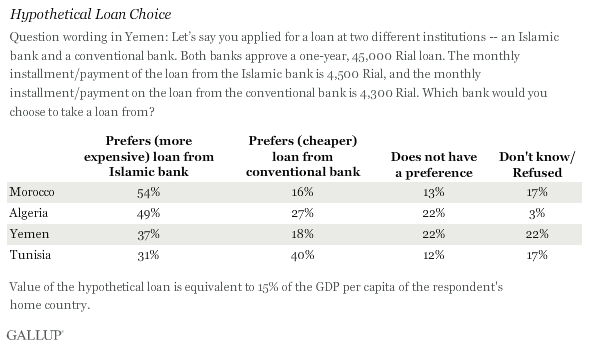

When confronted with a hypothetical scenario of taking out a loan from an Islamic bank with an effective 20% interest rate or a loan from a conventional bank with an effective interest rate of 15%, 45% of respondents prefer the more expensive Islamic bank loan. A proportion of 27% choose the cheaper, conventional loan and the rest do not have a preference.

Among the five countries surveyed, Moroccans are the most likely to choose the Sharia-compliant loan (54%), while Tunisians are the most likely to opt for the conventional loan (40%). Within each country, choices vary little among the poor and more affluent respondents. Men were more likely than women to choose the Islamic loan (48% vs. 43%), with the largest gender gap being observed in Egypt.

In reality, the price difference between a conventional and an Islamic loan is often less than five percentage points. The interest rate is presented in terms of the value of the monthly payment because explicit rates are not Sharia-compliant.

Implications

Islamic banking has become one the fastest growing segments in the international financial system and analysts expect it to maintain its rapid double-digit growth. Led by Malaysia and the countries forming the Gulf Cooperation Council, the global Islamic financial industry is now estimated to account for $1.4 to $1.7 trillion in assets, which is about 1% of total global financial assets. Worldwide the number of financial institutions has exceeded 600, operating in 75 countries.

Gallup's data show that few adults in Algeria, Egypt, Morocco, Tunisia, and Yemen currently use Islamic banking services. The data also suggest that in the Middle East and North Africa, , there is likely to be demand for both conventional and Islamic banking services.

Access the complete , , and at .

For complete data sets or custom research from the more than 150 countries 优蜜传媒continually surveys, please .

Survey Methods

Results are based on face-to-face interviews with 1,000 adults, aged 15 and older, conducted in 2012. For results based on the total sample of national adults, one can say with 95% confidence that the maximum margin of sampling error ranged from 卤3.4 percentage points to 卤3.6 percentage points at the 95% confidence level. The margin of error reflects the influence of data weighting. In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error or bias into the findings of public opinion polls.

In each of these five countries surveyed, with the exception of Egypt, 100% of respondents self-identified as Muslim. In Egypt, 95% of respondents did so. As a result of survey execution errors, the hypothetical loan choice summary statistics do not include data from Egypt. An important caveat is that these results are not representative of Islamic banking globally; in many countries, use of and attitudes toward Islamic finance are likely markedly different.

Exclusions

Morocco: Southern provinces were excluded.

Algeria: Sparsely populated areas in the far South were excluded, representing approximately 10% of the population.

Yemen: Shabwah and Abyan governorates were excluded because of security concerns. These areas represent approximately 5% of the total population.

For more complete methodology and specific survey dates, please review .

Demirguc-Kunt, A., and L. Klapper. Forthcoming. "Measuring Financial Inclusion: The Global Findex Database." Brookings Papers on Economic Activity.