This article is the second in a on payments and remittance behavior in South Asia and Indonesia highlighting results from a new 优蜜传媒study, "," funded by the Bill & Melinda Gates Foundation. Jake Kendall is a staff member of the Bill & Melinda Gates Foundation.

WASHINGTON, D.C. -- Adults in sub-Saharan Africa are more likely to use electronic means to send, bring, or receive remittances, money, payments, or transactions than are adults in South Asia and Indonesia. However, both populations represent largely untapped markets of potential consumers for formal money transfer services, with more than 342 million adults across these regions using only informal means to conduct such transactions in the 30 days prior to the survey.

These results, from a study of sub-Saharan African adults conducted in 2011, offer an in-depth look at the payments and remittance behaviors in 11 countries: Botswana, Democratic Republic of the Congo, Kenya, Mali, Nigeria, Rwanda, Sierra Leone, South Africa, Tanzania, Uganda, and Zambia. A 2012 study included Indonesia and six South Asian countries: Afghanistan, Bangladesh, India, Nepal, Pakistan, and Sri Lanka.

Both Regions Have Undeveloped Financial Markets

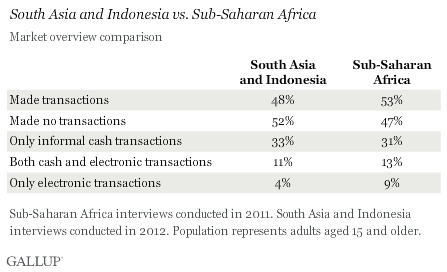

Pluralities of those in both regions who completed a transaction in the 30 days prior to the survey were most likely to do so by informal (cash-only) means, followed by using both electronic and cash payments, and lastly, only electronic (non-cash) means. These findings illustrate the underdevelopment of the market for financial services in each region.

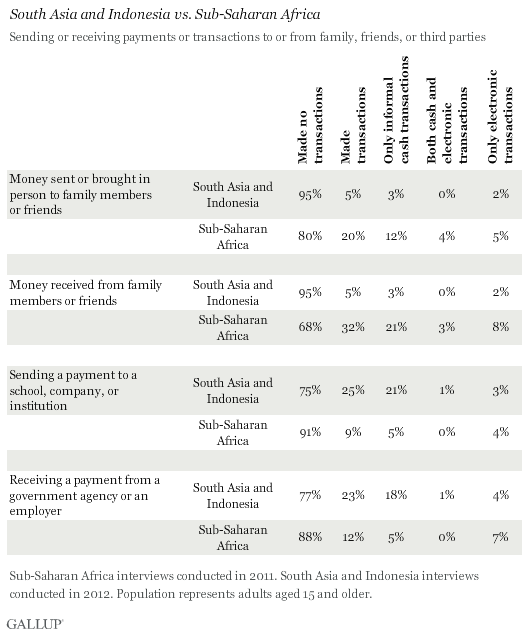

South Asians and Indonesians were less likely than respondents in the sub-Saharan African countries surveyed to send or receive payments to or from family or friends. Five percent of the total population surveyed in South Asia and Indonesia sent domestic remittances or payments to family or friends, and 5% received domestic remittances or payments from family or friends. In contrast, 20% of respondents in the sub-Saharan African countries surveyed reported sending a transaction, and 32% reported receiving one. A majority of those from both populations who sent or brought money to family or friends did so using informal cash payments.

South Asians and Indonesians were more likely than sub-Saharan Africans (25% vs. 9%) to send a payment to a school, institution, company, or other organization. A majority of senders from both regions used cash to send such payments.

Few adults in both regions engaged in international transactions. Almost no South Asians and Indonesians said they sent money to another country, and only 1% received a remittance from abroad. In the sub-Saharan African countries surveyed, 1% reported sending a remittance internationally while 3% reported receiving one.

Educated, Wealthy, and Young Largest Consumers of Electronic Transactions

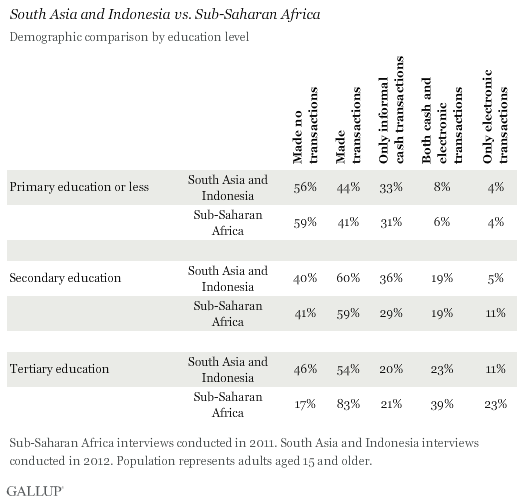

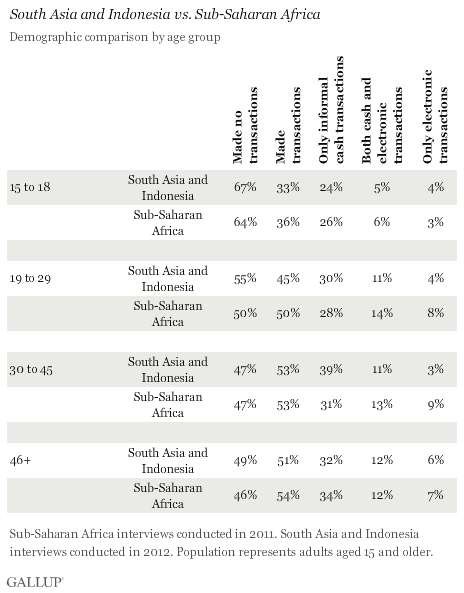

In both regions, those with tertiary education were more likely to use electronic means of money transfer than those with secondary or primary educations. Those with a primary education or less mostly used informal cash transfers.

In general, the young were less likely to make transactions than older respondents. Those aged 30 and older -- for whom employment peaks before declining with age -- were most likely to conduct transactions during the 30-day period before the survey.

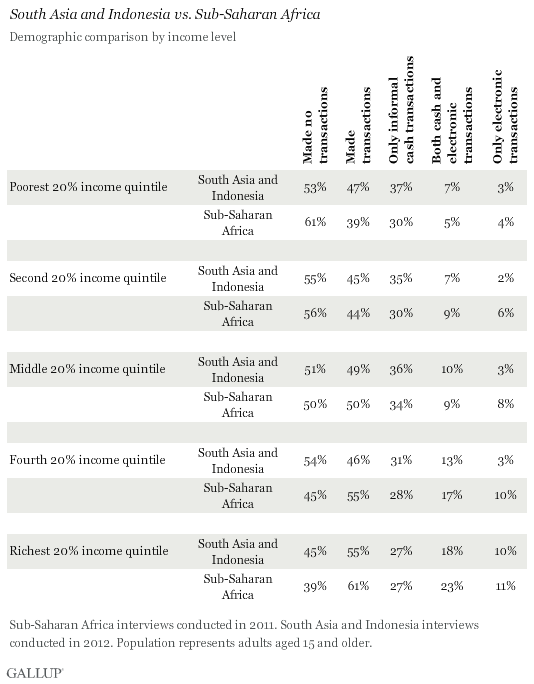

In both studies, the wealthiest 20% were most likely to have sent, brought, or received a money-based transaction in the 30 days prior to the survey. They were also more likely than any other group to use only electronic means to send or receive money. However, this group still used informal cash-based transfers more than any other method of sending or bringing money.

Implications

Both markets have similar levels of informal transaction activity. In sub-Saharan Africa, there is a total market of 134 million adult customers already making some form of money transfer or payment to another part of the country in cash. South Asia and Indonesia's untapped market is estimated to be more than 1.5 times as large, at 208 million adults.

Together, these regions' potential consumers of formal money transfer services account for approximately 5% of the global population. However, the remittance, transaction, and payment markets in sub-Saharan Africa may be slightly further along with the integration of electronic technologies (such as mobile phone banking) than their South Asian and Indonesian counterparts.

Mobile phone-based money services offer one of the most promising means of electronic banking in the developing world and have made major progress in the East African countries of Kenya, Tanzania, and Uganda in particular. In just a few short years, the global mobile money industry has grown significantly. Compared with 2007, when there were just a handful of mobile money deployments, there are now more than 100 worldwide, and 11 have more than a million registered users -- a large part of them in Africa. Despite this growth, the market is far from saturated. As the data show, the potential exists for hundreds of millions of additional consumers to become regular users of formal remittance and payments markets.

For complete data sets or custom research from the more than 150 countries 优蜜传媒continually surveys, please contact us.

Survey Methods

South Asia and Indonesia

Results are based on face-to-face interviews with 1,000 adults per country, aged 15 and older, conducted September-October 2012, in Indonesia, Afghanistan, Bangladesh, Nepal, Pakistan, and Sri Lanka, plus 2,540 adults in India. Regional totals represented in this article are population-weighted averages, accounting for the population size of a country. For results based on each sample of national adults, one can say with 95% confidence that the margin of sampling error was 卤1.26 percentage points. The margin of error reflects the influence of data weighting. In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error or bias into the findings of public opinion polls.

Sub-Saharan Africa

Results are based on face-to-face interviews with 1,000 adults per country, aged 15 and older, conducted June-October 2011, in Botswana, Democratic Republic of the Congo, Kenya, Mali, Nigeria, Rwanda, Sierra Leone, South Africa, Tanzania, Uganda, and Zambia. Regional totals presented in this article are population-weighted averages, accounting for the population size of a country. For results based on each sample of national adults, one can say with 95% confidence that the maximum margin of sampling error was 卤1.31 percentage points. The margin of error reflects the influence of data weighting. In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error or bias into the findings of public opinion polls.

There were the following exceptions for this study:

- In Democratic Republic of the Congo, North and South Kivu, Ituri, and Haut-Uele in the eastern part of the country were excluded due to insecurity. The excluded area represents approximately 20% of the population.

- In Uganda, the northern region was excluded due to the presence of LRA rebels. The excluded area represents approximately 10% of the population.

- The northern part of Mali, mainly extreme desert with difficult access and a nomadic population, was excluded. The excluded area represents 5% to 10% of the population.

- In Botswana and Zambia, the sample included a larger-than-expected proportion of respondents who reported completing a secondary education when compared to the data used for post-stratification weighting.