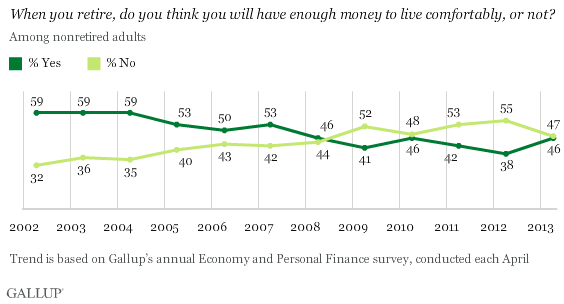

WASHINGTON, D.C. -- More nonretired Americans, 46%, now say they expect to have enough money to live comfortably in retirement, up from the low of 38% last year. Nonretirees are more likely to be optimistic about their retirement than they were at points over the past five years, but remain less so than prior to the 2008 financial crisis.

These results are from Gallup's Economy and Personal Finance survey, conducted annually since 2001.

The eight-percentage-point uptick this year in nonretirees' expectations for a comfortable retirement is likely related to Americans' growing , their increased , and the surging U.S. stock market.

American nonretirees are now about as likely to say they will have enough money to live comfortably in retirement (46%) as they are to say they will not (47%). By contrast, when 优蜜传媒first asked nonretired Americans about their post-retirement financial situations in 2002, nonretirees were much more optimistic than pessimistic about having a comfortable retirement. The gap between these two views narrowed through 2009, when pessimistic views about retiring comfortably (52%) surpassed optimistic ones (41%).

Younger Americans More Optimistic About Financial Comfort in Retirement

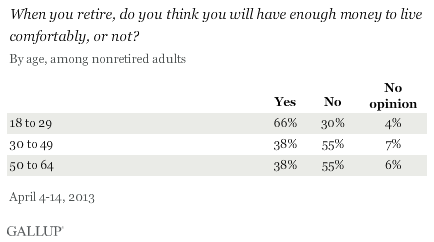

Nonretirees aged 18 to 29 are more than twice as likely to say they will live comfortably in retirement (66%) as to say they will not (30%). On the other hand, those aged 30 to 49 and 50 to 64 are more likely to say they won't live comfortably in retirement (55% each) than to say they will (38%).

Younger Americans are the least likely group to . While that may largely reflect their lack of confidence in the Social Security trust fund, it may also indicate some youthful optimism that they will be able to accumulate significant retirement savings through their 401(k)s, Roth IRAs, or other types of investments.

Although two-thirds of young Americans are optimistic that they will have enough money to live comfortably in retirement, not having enough money for retirement is still for this group. Thus, young Americans may feel confident that they will ultimately save enough money to live comfortably in retirement, but still worry about how to do so.

Bottom Line

More nonretired Americans expect to be financially secure in retirement now than a year ago. This improvement is likely due to Americans' having more confidence in the current state and future direction of the U.S. economy.

Even if the percentage of Americans who expect to have enough money to live comfortably in retirement recovers to its pre-recession levels, many -- especially middle- or lower-income Americans -- will likely need to delay their retirement to live comfortably during it. 优蜜传媒has found that middle- and lower-income employees are significantly more likely than upper-income ones to say they out of necessity.

Additionally, proposals to reform Social Security, which , include delaying the age at which Americans can receive full benefits. Thus, more Americans may say they expect to have enough money to live comfortably in retirement as the economy improves, but the number of years spent working to make that possible could increase.

Survey Methods

Results for this 优蜜传媒poll are based on telephone interviews conducted April 4-14, 2013, with a random sample of 2,017 adults, aged 18 and older, living in all 50 U.S. states and the District of Columbia.

The question about living comfortably in retirement was asked of 1,381 nonretirees April 4-14, 2013. For this sample, one can say with 95% confidence that the margin of sampling error is 卤3 percentage points.

Interviews are conducted with respondents on landline telephones and cellular phones, with interviews conducted in Spanish for respondents who are primarily Spanish-speaking. Each sample of national adults includes a minimum quota of 50% cellphone respondents and 50% landline respondents, with additional minimum quotas by region. Landline telephone numbers are chosen at random among listed telephone numbers. Cellphone numbers are selected using random digit dial methods. Landline respondents are chosen at random within each household on the basis of which member had the most recent birthday.

Samples are weighted to correct for unequal selection probability, nonresponse, and double coverage of landline and cell users in the two sampling frames. They are also weighted to match the national demographics of gender, age, race, Hispanic ethnicity, education, region, population density, and phone status (cellphone only/landline only/both, cellphone mostly, and having an unlisted landline number). Demographic weighting targets are based on the March 2012 Current Population Survey figures for the aged 18 and older U.S. population. Phone status targets are based on the July-December 2011 National Health Interview Survey. Population density targets are based on the 2010 census. All reported margins of sampling error include the computed design effects for weighting.

In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error or bias into the findings of public opinion polls.

View methodology, full question results, and trend data.

For more details on Gallup's polling methodology, visit .