This post is part of Gallup's ongoing series on the shifting landscape for financial institutions. It provides insights into channel optimization, emerging customer behaviors and preferences, product penetration and relationship growth, engaging the most critical affluent and business customers, and reshaping banks' overall value proposition.

Let me set the stage for you: It's a big meeting, your marketing and field leadership have gathered. Some sit in a conference room around a large table, while others join via a phone that is set out in the middle of the table. The head of your customer experience team is presenting the results of your latest competitive market study. The numbers are not where you expected them to be. Once again, consumer perception of your bank is not great -- it falls in the middle or bottom of the pack. Now the finger pointing starts. It's subtle at first, but everyone is looking for the silver bullet answer that deflects responsibility from their group.

- It's the branches' fault because wait times are up.

- It's the call center's fault because customer satisfaction is down.

- It's product's fault because we are behind the curve on mobile features.

- Compliance is too conservative.

- Advertising doesn't speak to millennials.

- Wealth management has no strategy.

- HR can't hire good people fast enough.

- IT hasn't fixed the teller transaction system.

- We're not doing enough community outreach.

- We don't have a differentiated brand.

- We need to drive more people into the branch.

- We need to drive more people into digital channels.

- There aren't enough cross sales because if our customers just used more of our stuff they would definitely like us more.

The atmosphere is getting increasingly tense and desperate, and then someone hits on it -- it's not our fault. Consumers don't like banks these days and there's nothing we can do about it. The banks that consistently show up at the top of all the customer satisfaction surveys aren't doing anything better than us, they are just outliers in an industry that people hate. Phew, responsibility denied and dissolved.

With so much banter in the media about how little people think of the banking industry, it can be easy for individual banks to sidestep responsibility for their less-than-stellar image. Leaders commonly make excuses along the lines of: "There's nothing more we can do, everyone hates banks," "We are suffering just like others in the industry," or "It is better than 2008, but we're not back to the good times yet."

Yet the latest 优蜜传媒Retail Banking study shows that while only 33.8% of people are satisfied with the banking industry overall, 80.5% are satisfied with their primary bank. And 49.3% of people who are satisfied with their primary bank are not satisfied with the industry.

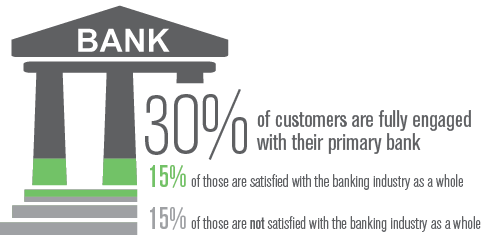

But we all know that satisfaction is not enough. Customer engagement is the true driving force behind financial outcomes. According to the same retail banking study, 30% of the market is fully engaged with their primary bank. And it turns out that 15% of those same customers are satisfied with the banking industry as a whole and 15% are not. It is perfectly possible -- and highly probably -- to be satisfied or engaged with your primary bank but still not like the banking industry as a whole.

It is 2015 -- no more perception-related excuses. Get out there and start making the tough decisions necessary to improve your customer engagement. Every department has blame to own and every department has a responsibility to fix what they have control over. It's time to set the stage for a different conversation in 2016.